This counseling session, which typically costs around $125, should take a minimum of 90 minutes and need to cover the advantages and disadvantages of getting a reverse home loan given your unique monetary and personal scenarios. It needs to discuss how a reverse home loan might affect your eligibility for Medicaid and Supplemental Security Earnings.

Your obligations under the reverse mortgage guidelines are to remain current on real estate tax and property owners insurance and keep the home in excellent repair work. And if you stop living in your house for The original source longer than one yeareven if it's since you're residing in a long-lasting care center for medical reasonsyou'll need to repay the loan, which is usually achieved by offering your home.

Regardless of recent reforms, there are still scenarios when a widow or widower might lose the home upon their partner's death. The Department of Housing and Urban Development changed the insurance coverage premiums for reverse home loans in October 2017. Because lenders can't ask homeowners or their successors to pay up if the loan balance grows bigger than the home's value, the insurance premiums offer a swimming pool of funds that lenders can draw on so they don't lose cash when this does take place.

The up-front premium utilized to be tied to how much customers got in the first year, with house owners who got the mostbecause they required to settle an existing mortgagepaying the greater rate. Now, all debtors pay the very same 2.0% rate. The up-front premium is computed based on the house's worth, so for each $100,000 in evaluated worth, you pay $2,000.

All customers need to also pay annual home loan insurance premiums of 0.5% (previously 1.25%) of the quantity obtained. This change conserves borrowers $750 a year for each $100,000 borrowed and assists offset the higher up-front premium. It also implies the customer's debt grows more slowly, preserving more of the homeowner's equity in time, providing http://messiahputq265.lowescouponn.com/h1-style-clear-both-id-content-section-0-the-basic-principles-of-what-is-the-interest-rate-on-reverse-mortgages-h1 a source of funds later in life or increasing the possibility of being able to pass the home down to successors.

Reverse home loans are a specialty product, and only particular lending institutions provide them. Some of the greatest names in reverse home loan loaning consist of American Advisors Group, One Reverse Home Mortgage, and Liberty Home Equity Solutions. It's a great idea to request a reverse home loan with a number of companies to see which has the most affordable rates and fees.

How Many Types Of Reverse Mortgages Are There for Beginners

Just the lump-sum reverse home loan, which gives you all the profits at the same time when your loan closes, has a set rates of interest. The other 5 options have adjustable interest rates, which makes sense, given that you're borrowing cash over several years, not simultaneously, and interest rates are constantly changing.

In addition to among the base rates, the lending institution adds a margin of one to 3 portion points. So if LIBOR is 2.5% and the lending institution's margin is 2%, your reverse home loan rates of interest will be 4.5%. Check out this site Since Jan. 2020, loan providers' margins ranged from 1.5% to 2.5%. Interest substances over the life of the reverse home loan, and your credit rating does not affect your reverse home loan rate or your capability to qualify.

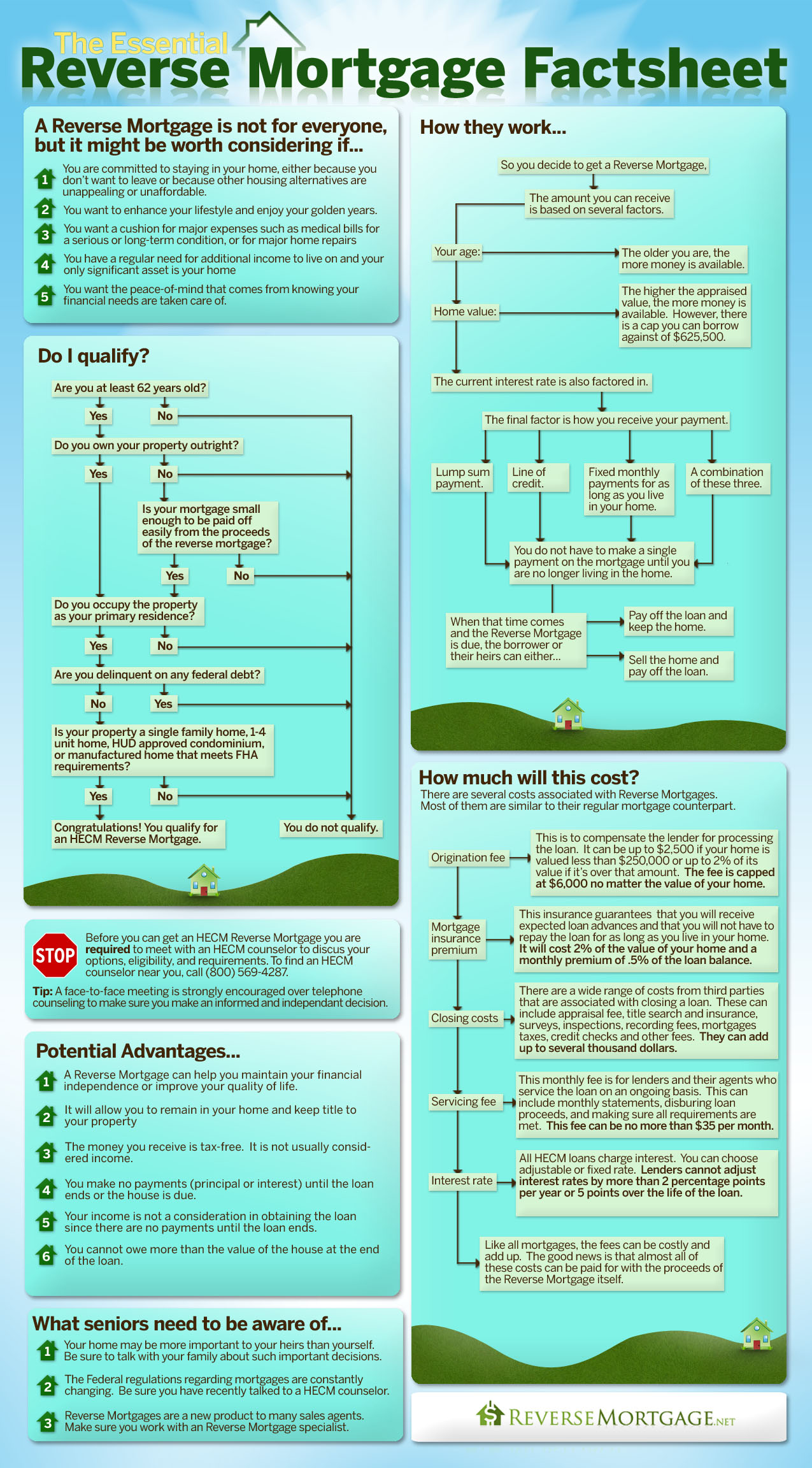

For a HECM, the amount you can obtain will be based upon the youngest borrower's age, the loan's interest rate, and the lower of your house's appraised worth or the FHA's optimum claim quantity, which is $765,600 since Jan. 1, 2020. You can't obtain 100% of what your home deserves, or anywhere near to it, however (when did 30 year mortgages start).

Here are a couple of other things you need to know about just how much you can obtain: The loan proceeds are based on the age of the youngest debtor or, if the customer is wed, the more youthful partner, even if the younger partner is not a debtor. The older the youngest borrower is, the higher the loan earnings.

The higher your residential or commercial property's appraised worth, the more you can borrow. A strong reverse mortgage monetary evaluation increases the profits you'll receive due to the fact that the loan provider will not keep part of them to pay property taxes and house owners insurance on your behalf. The quantity you can in fact borrow is based on what's called the preliminary principal limit.

The federal government decreased the preliminary primary limitation in October 2017, making it harder for property owners, particularly younger ones, to receive a reverse home loan. On the upside, the modification assists debtors maintain more of their equity. The government decreased the limitation for the same reason it altered insurance coverage premiums: due to the fact that the home mortgage insurance fund's deficit had actually nearly doubled over the past fiscal year.

The Best Strategy To Use For How Much Do Mortgages Cost Per Month

To further make complex things, you can't borrow all of your initial primary limitations in the very first year when you pick a swelling amount or a line of credit. Rather, you can obtain approximately 60%, or more if you're utilizing the money to settle your forward mortgage. And if you choose a lump amount, the amount you get up front is all you will ever get.

Both partners have to consent to the loan, but both don't have to be customers, and this arrangement can produce problems. If two spouses live together in a home but just one partner is called as the debtor on the reverse mortgage, the other spouse is at threat of losing the house if the loaning spouse passes away initially.

If the making it through spouse desires to keep the home, she or he will need to repay the loan through other means, potentially through an expensive refinance. Just one partner might be a debtor if only one spouse holds title to your home, maybe due to the fact that it was acquired or since its ownership predates the marriage.

The nonborrowing spouse might even lose the house if the borrowing spouse had to move into a nursing home or nursing house for a year or longer. With an item as possibly lucrative as a reverse mortgage and a vulnerable population of borrowers who might have cognitive impairments or be desperately looking for financial redemption, scams abound.

The vendor or professional may or might not in fact provide on promised, quality work; they might simply take the property owner's cash. Family members, caretakers, and financial consultants have actually likewise taken benefit of seniors by using a power of lawyer to reverse mortgage the house, then taking the profits, or by convincing them to purchase a financial item, such as an annuity or entire life insurance coverage, that the senior can only pay for by obtaining a reverse home loan.

These are simply a few of the reverse mortgage rip-offs that can trip up unwitting homeowners. Another risk related to a reverse home mortgage is the possibility of foreclosure. Although the debtor isn't accountable for making any home loan paymentsand for that reason can't become overdue on thema reverse home mortgage needs the debtor to satisfy particular conditions.

10 Simple Techniques For Who Does Usaa Sell Their Mortgages To

As a reverse mortgage customer, you are needed to reside in the home and maintain it. If the home falls into disrepair, it won't be worth reasonable market price when it's time to offer, and the loan provider won't have the ability to recoup the full quantity it has actually encompassed the customer.